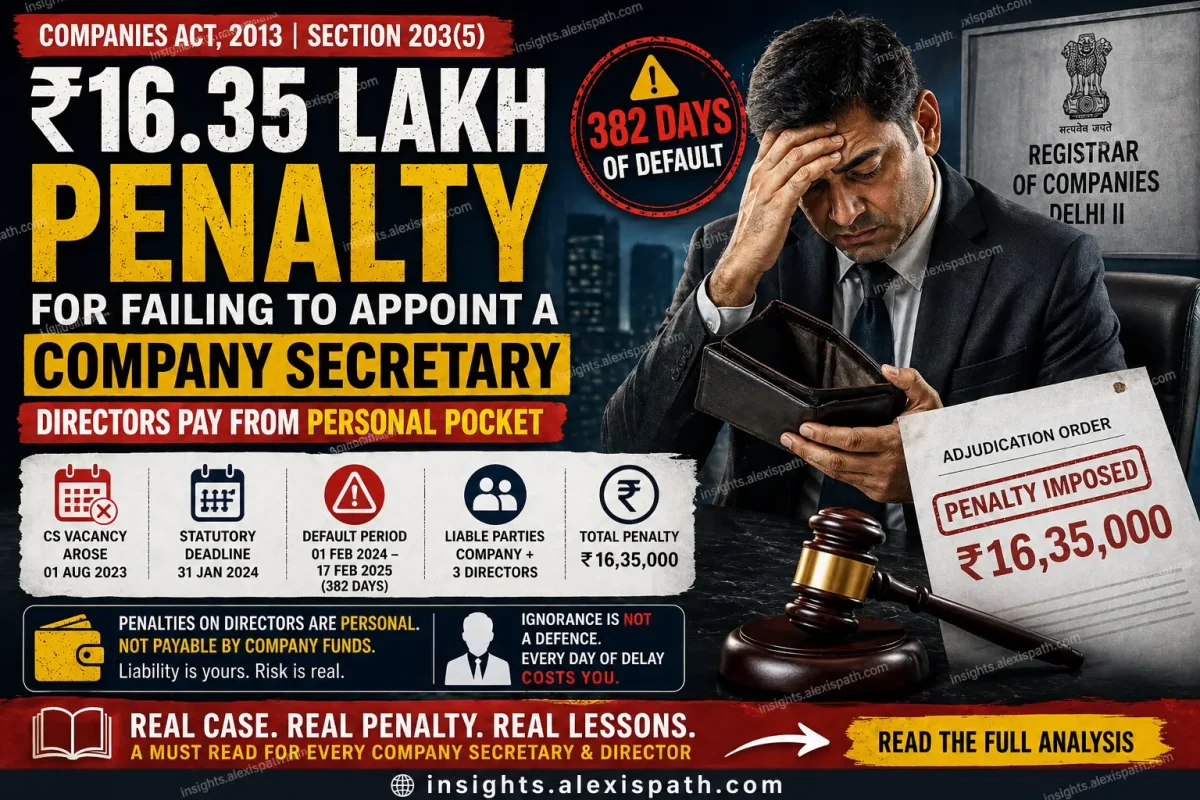

An analysis of adjudication order No. PO/ADJ/04-2026/DC/01934 dated 15th April 2026, issued by the Registrar of Companies, Delhi II against FS India Devco Private Limited and its directors for violation of Section 203(5) of the Companies Act, 2013.

Abstract — This article analyses the adjudication order dated 15th April 2026 in which the Registrar of Companies, Delhi II imposed aggregate penalties of ₹16,35,000 on FS India Devco Private Limited and three of its directors for a 382-day delay in appointing a whole-time Company Secretary following a vacancy. Written from a Company Secretaryship student perspective, the article explains the statutory mandate under Section 203 of the Companies Act, 2013, dissects the penalty computation, examines key legal principles emerging from the order, and draws actionable compliance lessons for practising and aspiring Company Secretaries.

1. Introduction

The office of a Company Secretary (CS) under the Companies Act, 2013 is not merely an administrative role — it is a statutory cornerstone of corporate governance in India. Section 203 of the Act mandates that every company belonging to a prescribed class must appoint a whole-time Key Managerial Personnel (KMP), which includes a Company Secretary. The law further prescribes strict timelines for filling any vacancy in such positions and backs non-compliance with substantial financial penalties.

The adjudication order dated 15th April 2026, bearing Order No. PO/ADJ/04-2026/DC/01934, issued by the Registrar of Companies (ROC), Delhi II against FS India Devco Private Limited and three of its directors, is an important reminder that non-compliance with these provisions attracts penalties that accumulate daily. The total penalty imposed in this single proceeding amounts to ₹16,35,000 — a sum that could have been entirely avoided with timely action. This case is particularly instructive because the default arose not from deliberate non-compliance but from a seemingly routine event: the resignation of the incumbent Company Secretary.

For students pursuing the Company Secretaryship course, this case provides an invaluable real-world lens through which to understand the interplay of statutory duty, corporate accountability, and regulatory enforcement under the modern company law framework in India.

2. Statutory framework: Section 203, Companies Act 2013

2.1 Who must appoint a Company Secretary?

Section 203(1) of the Companies Act, 2013 requires every listed company and every other public company with a paid-up share capital of ten crore rupees or more to appoint the following whole-time Key Managerial Personnel:

- A Managing Director, Chief Executive Officer, Manager, or Whole-time Director

- A Company Secretary

- A Chief Financial Officer

For private companies, Rule 8A of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 extends the same obligation to every private company which has a paid-up share capital of ten crore rupees or more. FS India Devco Private Limited, being a private company, fell within this rule's ambit.

2.2 The six-month rule for vacancies: Section 203(4)

Section 203(4) stipulates that if the office of any whole-time KMP falls vacant for any reason, the resulting vacancy must be filled by the Board of Directors at a Board meeting within a period of six months from the date of such vacancy. This is not a directory provision that a company can treat as advisory — it is a mandatory statutory obligation backed by financial penalty under Section 203(5).

The six-month window is intended to give companies a reasonable transition period without leaving a critical governance position unstaffed indefinitely. However, as this case demonstrates, companies often allow the transition period to stretch far beyond what the law permits.

2.3 Penalty for non-compliance: Section 203(5)

Section 203(5) prescribes the following penalty structure for any default in complying with the provisions of Section 203:

- Company: ₹5,00,000 (flat penalty)

- Every director and KMP in default: ₹50,000 as a base penalty

- Continuing default: An additional ₹1,000 per day for each day the default continues beyond the first

- Maximum cap on the continuing default penalty: ₹5,00,000 per person

For a default lasting 382 days, a director's penalty works out to: ₹50,000 (base) + (382 × ₹1,000) = ₹4,32,000. The penalty grows by ₹1,000 for each day of inaction, making delay exponentially more expensive than the cost of proactive compliance.

3. Case background: FS India Devco Private Limited

3.1 About the company

FS India Devco Private Limited is incorporated under the Companies Act, 2013 with its registered office at 808, 8th Floor, Narain Manzil, 23, Barakhamba Road, New Delhi — 110001 (CIN: U40102DL2013PTC338399). The CIN prefix U40102 indicates the company's principal business activity falls under electricity, gas, steam, and air conditioning supply — suggesting it is an energy sector entity, likely an Indian subsidiary or project company associated with a multinational group.

3.2 Key Facts at a Glance

| Parameter | Detail |

|---|---|

| CS vacancy arose | 01 Aug 2023 |

| Resignation of | Ms. Rupa Vijay |

| Statutory deadline | 31 Jan 2024 |

| 6-month window expires | — |

| Default period | 382 days |

| Period | 01 Feb 2024 – 17 Feb 2025 |

| Total penalty | ₹16,35,000 |

| Liable parties | Company + 3 directors |

3.3 Chronology of events

| Date | Event |

|---|---|

| 01.08.2023 | Company Secretary Ms. Rupa Vijay resigns from the company |

| 31.01.2024 | Statutory deadline: CS must be appointed (6 months from 01.08.2023) — deadline missed |

| 01.02.2024 | Default commences; continuing penalty clock begins ticking at ₹1,000/day per director |

| 09.09.2024 | Director Diana Michael Sequeira resigns — her personal default period ends at 221 days |

| 17.02.2025 | Ms. Avneet Kaur Oberoi appointed as Company Secretary — default ends after 382 days |

| 10.03.2025 | DIR-12 filed (SRN AB2888078) for CS appointment |

| 30.04.2025 | Company files GNL-1 application for compounding of penalty (SRN N30515316) |

| 17.12.2025 | Regional Director redirects application to ROC for adjudication |

| 04.02.2026 | e-SCN (electronic Show Cause Notice) issued to company and all officers in default |

| 11.02.2026 | Company submits reply to the Show Cause Notice |

| 15.04.2026 | ROC Delhi II passes final adjudication order imposing penalties of ₹16,35,000 |

4. Penalty computation and analysis

4.1 Detailed penalty breakdown

| Person / entity | Default days | Penalty calculation | Penalty imposed |

|---|---|---|---|

| FS India Devco Pvt. Ltd. | — | Flat statutory maximum for company | ₹5,00,000 |

| Himanshu Jangid, Director (DIN: 08254587) | 382 | ₹50,000 + (382 × ₹1,000) = ₹4,32,000 | ₹4,32,000 |

| Nitin Grover, Director (DIN: 09746681) | 382 | ₹50,000 + (382 × ₹1,000) = ₹4,32,000 | ₹4,32,000 |

| Diana Michael Sequeira, Director* (DIN: 07286067) | 221 | ₹50,000 + (221 × ₹1,000) = ₹2,71,000 | ₹2,71,000 |

* Diana Michael Sequeira resigned as director on 09.09.2024. Her liability is computed only for the period she held office: 01.02.2024 to 09.09.2024 (221 days).

4.2 Why did Diana Sequeira pay less?

The company's reply to the Show Cause Notice correctly pointed out that Ms. Sequeira had tendered her resignation from the directorship on 09.09.2024, well before the default was rectified on 17.02.2025. The Adjudicating Officer accepted this submission and computed her penalty only for the 221-day period during which she was a director and the default was simultaneously ongoing.

This reflects a fundamental principle of regulatory accountability: liability must correspond to the period of culpability. A person cannot be held responsible for a continuing default during a period when she no longer held the office that gave rise to the obligation.

4.3 Rejection of the remission plea

The company, in its reply, submitted that the delay was inadvertent and arose from the transition period following the resignation of the erstwhile CS. It requested remission (reduction) of the penalty on grounds of good faith and subsequent corrective action. The Adjudicating Officer did not accept this submission and explicitly declined to grant any remission.

The order makes clear that the inadvertence of a default does not automatically entitle a company to remission. The Adjudicating Officer exercises independent discretion. Companies should never treat remission as a risk management strategy or a fallback option — prevention is always cheaper than adjudication.

5. Key legal principles from this order

5.1 The continuing default principle

The concept of a "continuing default" is central to this case. Unlike a one-time violation where a flat penalty is imposed, the failure to appoint a CS accrues penalties on a daily basis from the day following the statutory deadline. At ₹1,000 per director per day, the financial exposure grows rapidly: at 100 days, each director owes ₹1,50,000; at 200 days, ₹2,50,000; at 382 days, ₹4,32,000.

This structure is deliberately designed to incentivise prompt corrective action. The message from Parliament is unambiguous: the longer a company delays filling a mandatory KMP vacancy, the more painful the financial consequence.

5.2 Director liability is personal and cannot be indemnified

The order specifically directs that the penalty imposed on officers in default shall be paid from their personal sources and income. This is not a procedural nicety — it is a substantive restriction. A company cannot, as a matter of law or policy, reimburse directors for penalties imposed on them personally under the Companies Act, 2013.

This means that every director sitting on the board of a company that defaults on a KMP appointment obligation is personally exposed to a potentially significant financial liability. Non-executive directors, independent directors, and nominee directors are not immune — if they are directors during the period of default and are "officers in default" under the Act, they are equally liable.

5.3 Resignation does not extinguish liability for the period of default

Diana Sequeira's case establishes an important nuance that every CS student must internalise: a director who resigns during the currency of a default is still personally liable for the period she held office. The fact that she resigned long before the default was rectified did not absolve her of liability for the 221 days she was a director during the default period.

The implication is clear: if a director discovers that the company has failed to fill a mandatory KMP vacancy beyond the statutory deadline, the appropriate response is not to quietly resign and await the end of proceedings — it is to actively agitate at the Board level for immediate corrective action.

5.4 Compounding is not always available — adjudication may be required

The company initially sought to compound the offence under Section 441 of the Act by filing a GNL-1 application before the Regional Director. However, the Regional Director redirected the matter to the ROC for adjudication under Section 454. This reflects an important procedural distinction: compounding under Section 441 is available for offences punishable by fine only; the Adjudicating Officer under Section 454 is separately empowered to impose penalties. Where the RD determines that adjudication is more appropriate, compounding will not be granted.

5.5 Mandatory Board Report disclosure

The order conditions the imposition of penalty on the requirement that the penalty be disclosed in the company's forthcoming Board Report. This flows from Section 134 of the Companies Act, 2013, which mandates transparency in Board reporting. Shareholders, creditors, and other stakeholders have a right to know when a company has attracted a regulatory penalty of this magnitude. CS professionals must ensure such disclosures are made accurately and in the appropriate financial year.

7. Post-order obligations and consequences of non-compliance

7.1 Payment of penalty: 90-day deadline

All notified officers in default are required to pay the penalty within 90 days of receipt of the adjudication order. Payment must be made through the e-Adjudication portal on the MCA website using respective login IDs. Proof of payment (challan or SRN) must be uploaded on the portal. As noted above, the payment must come from the director's personal sources — company funds cannot be used to discharge personal penalties.

7.2 Right of appeal

Any person aggrieved by this adjudication order may file an appeal in Form ADJ before the Regional Director (RD Delhi) within 60 days of the date of receipt of the order, in terms of Section 454(5) and 454(6) of the Companies Act, 2013 read with the Companies (Adjudication of Penalties) Rules, 2014. The appeal must clearly set out the grounds of challenge and must be accompanied by a certified copy of the order.

7.3 Consequences of non-payment: Section 454(8)

Section 454(8) of the Companies Act, 2013 provides that failure to pay the adjudicated penalty within the prescribed period renders the company and defaulting officers liable to imprisonment for a term which may extend to six months, or a fine of not less than ₹25,000 extendable to ₹5,00,000, or both. Paying the adjudicated penalty on time is therefore not optional — it is a legal obligation with criminal consequences for default.

8. Lessons and Best Practices for Company Secretaries

| # | Lesson | Actionable Insight |

|---|---|---|

| 01 | Maintain a live KMP vacancy tracker | Proactively track the tenures and potential exit risks of all KMP positions. Set calendar alerts at 90, 60, and 30 days before the 6-month statutory deadline for every vacancy. |

| 02 | Trigger recruitment on day one of vacancy | Upon any KMP resignation, alert the Board immediately and commence a formal recruitment process. Do not wait for the dust to settle — the 6-month clock starts on day one. |

| 03 | Minute the urgency formally | Board minutes must reflect the urgency of filling the KMP vacancy, with specific resolutions delegating the search to a committee or HR with a defined timeline and accountability. |

| 04 | Do not treat compounding as a safety net | As this case shows, the RD may redirect a compounding application to the ROC for adjudication. Compounding is not an automatic remedy — prevention is the only reliable one. |

| 05 | Disclose fully in the Board Report | Penalties imposed by regulators must be accurately disclosed in the Board Report under Section 134. Suppression of material regulatory actions creates further legal exposure. |

| 06 | Advise every director on personal liability | A CS is the conscience of the Board. All directors — executive, non-executive, independent, nominee — must understand that KMP vacancy defaults carry personal, non-indemnifiable financial liability. |

9. Conclusion

The adjudication order against FS India Devco Private Limited and its directors is a powerful illustration of the financial and governance consequences of treating mandatory statutory obligations as administrative afterthoughts. A 382-day delay in filling a CS vacancy — arising from the entirely foreseeable event of a resignation — cost the company and its directors a combined ₹16,35,000 in penalties, in addition to the significant management time spent navigating the regulatory process over more than a year.

The order reinforces three bedrock principles of company law compliance: that statutory mandates are not aspirational targets but enforceable obligations; that directors carry personal, non-delegable accountability for governance failures on their watch; and that the passage of time, far from erasing a default, makes it more expensive with every passing day.

For Company Secretaryship students and practitioners, the most important takeaway is this: the Company Secretary is uniquely positioned — by training, by statutory role, and by proximity to the Board — to prevent exactly this kind of default. A well-designed compliance calendar, a proactive relationship with the Board, and the professional courage to raise red flags in time are not just good practices. They are the essence of what it means to be a Company Secretary in India today.

"The Companies Act, 2013 leaves no room for inadvertence when it comes to mandatory KMP appointments. Every default has a cost — and that cost is borne by people."