An analysis of ROC Hyderabad's Adjudication Order No. PO/ADJ/04-2026/HD/02037 dated 22nd April 2026

Introduction: Why This Order Matters to Every CS Student

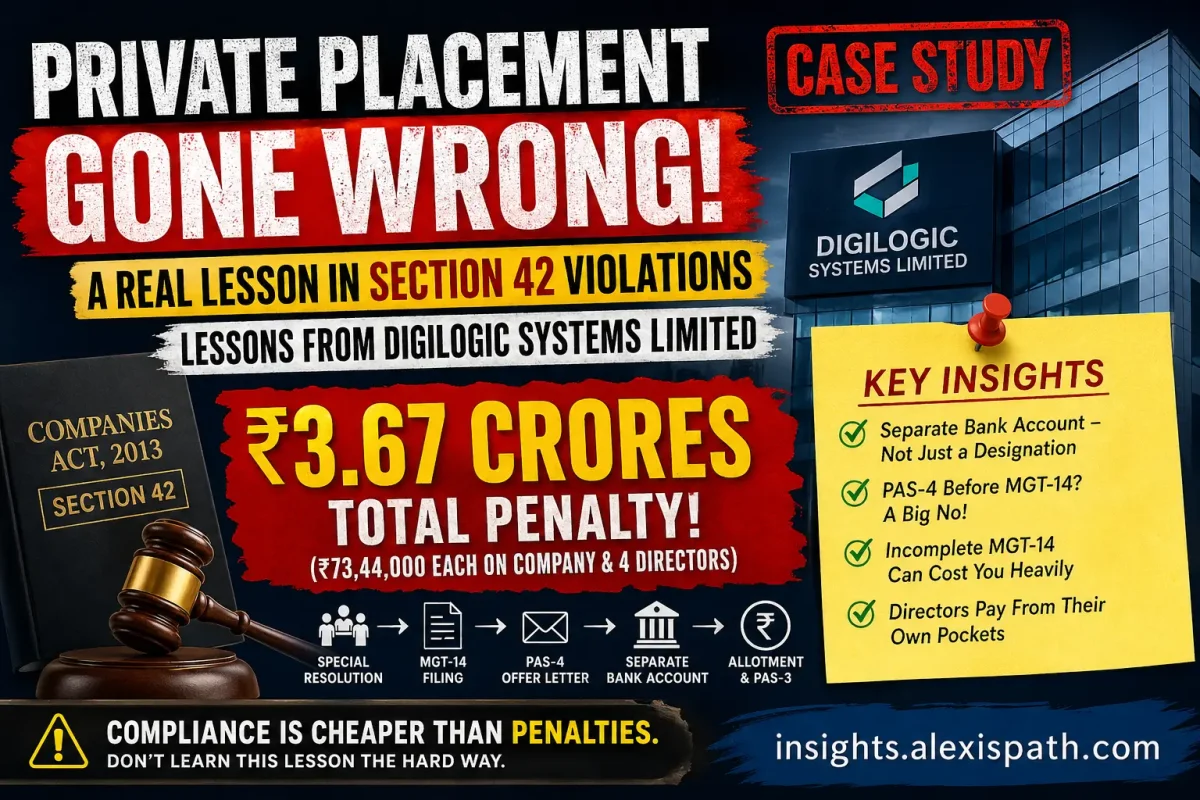

As a Company Secretary student, you will spend countless hours studying the theoretical provisions of the Companies Act, 2013. You will memorise sections, rules, and penalties. But nothing brings those provisions alive quite like a real adjudication order — one where a company, its directors, and its promoters are staring at a penalty of Rs. 73,44,000 each, totalling over Rs. 3.67 crores collectively, for what the company itself described as a "minor" compliance lapse.

The adjudication order issued by ROC Hyderabad against M/s Digilogic Systems Limited is one such case. It is not a story of deliberate fraud. It is not a story of an unscrupulous promoter running away with investor money. It is, in fact, a story of a company that was preparing for its IPO, hired professionals for due diligence, discovered compliance gaps, and still ended up paying a steep price. That, in itself, is the most important lesson.

Let us dissect this order thoroughly.

Part I: Who Is Digilogic Systems Limited?

Digilogic Systems Limited (CIN: U62099TG2011PLC077933) is a company registered with the Registrar of Companies, Hyderabad, under the Companies Act. Its registered office is situated at DSL Abacus Tech Park, Uppal, Hyderabad, Telangana.

The company was seemingly on an exciting growth trajectory — it was in the pre-IPO stage, undergoing due diligence for a public issue. This is significant context. Companies preparing for an IPO undergo intense legal and secretarial scrutiny. Every past transaction is examined under a microscope. And it was precisely this scrutiny that exposed the compliance gaps that led to this order.

The officers in default in this matter are:

- Madhusudhan Varma Jetty (DIN: 02247769) — appears to be the key promoter/director

- Radhika Varma Jetty (DIN: 03370284)

- Jetty Shashank Varma (DIN: 03370303)

- Hitesh Varma Jetty (DIN: 10648537)

The family nature of the directorial composition is evident. All four individuals share the same residential address, suggesting this is a closely held, family-promoted company — a very common structure among companies preparing for an SME IPO.

Part II: What Did the Company Actually Do — The Transaction in Question

To understand the violation, you must first understand what the company did. Here is a step-by-step reconstruction of the transaction:

1. Decision to raise funds via private placement: The company passed a special resolution on 12th February 2025 for private placement of equity shares.

2. The size of the allotment: The company decided to allot 25,000 equity shares of Rs. 10/- each at a premium of Rs. 283.76/- per share. Total amount raised: Rs. 73,44,000/- (25,000 × Rs. 293.76 = Rs. 73,44,000).

3. Allotment: The shares were allotted to one identified investor on 14th February 2025 — just two days after the special resolution. This was the third tranche of private placement by the company.

4. PAS-3 filing: The Return of Allotment (Form PAS-3, SRN: AB2773353) was filed on 21st February 2025 — within the prescribed timeline.

5. MGT-14 filing: Here is where things got complicated. The company filed Form MGT-14 (for special resolutions) with SRN AB2715690, dated 14th February 2025, taken on record by MCA on 19th February 2025. However, this filing had an incomplete explanatory statement as required under Rule 13 of the Companies (Share Capital and Debentures) Rules, 2014 and Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014. The company later filed a revised MGT-14 (SRN: AB4513078) with complete disclosures, which was taken on record as late as 11th June 2025 — nearly four months after the allotment.

6. PAS-4 timing issue: The company circulated the Private Placement Offer Letter (Form PAS-4) dated 12th February 2025 before filing Form MGT-14. This is a procedural irregularity as the offer letter should follow the proper filing sequence.

7. The separate bank account issue: This is the central violation. Section 42(6) of the Companies Act, 2013 mandates that monies received on application under a private placement shall be kept in a separate bank account in a scheduled bank. The company did not open a new separate bank account. Instead, it designated one of its existing bank accounts (other than its regular cash credit account) as the designated account for receiving share application money.

Part III: The Legal Framework — Understanding Section 42

Before we analyse the violation, let us clearly understand the statutory provisions involved. This is absolutely essential for any CS student.

Section 42 — Private Placement

Section 42 of the Companies Act, 2013 governs the process of private placement of securities. A private placement means any offer or invitation to subscribe to securities made to a select group of persons (not more than 200 in a financial year, excluding Qualified Institutional Buyers and employees).

Section 42(6) lays down the following obligations:

- The company must allot securities within 60 days from the date of receipt of application money.

- If unable to allot within 60 days, the company must refund the application money within 15 days from the expiry of those 60 days.

- If it fails to refund even then, interest at 12% per annum is payable from the 61st day.

- Most critically: Monies received on application must be kept in a separate bank account in a scheduled bank and shall not be used for any purpose other than (a) adjustment against allotment of securities, or (b) repayment of monies where allotment cannot be made.

Section 42(10) — the penalty provision:

"Subject to sub-section (11), if a company makes an offer or accepts monies in contravention of this section, the company, its promoters and directors shall be liable for a penalty which may extend to the amount raised through the private placement or two crore rupees, whichever is lower."

Additionally, the company must also refund all monies with interest as specified in sub-section (6) to subscribers within 30 days of the order imposing the penalty.

This is a very important penalty structure — it is not a fixed penalty. It is calibrated to the amount raised, subject to a ceiling of Rs. 2 crores. So in this case, since Rs. 73,44,000 is lower than Rs. 2 crores, the penalty per person is Rs. 73,44,000.

Part IV: The Violations — What Went Wrong

Based on the adjudication order, the following violations were established:

Violation 1: No Separate Bank Account (Primary Violation)

This is the core contravention of Section 42(6). The law uses very clear language: monies shall be kept in a separate bank account. The company's defence was that it had designated an existing account (other than its regular cash credit account) specifically for receiving share application money, and had even intimated Axis Bank of this designation in its board meeting dated 14th September 2024.

The company argued — supported by an opinion from a Practising Company Secretary (PCS) — that "separate bank account" does not necessarily mean a new bank account. However, the Adjudicating Officer was not convinced by this argument and held that the contravention under Section 42(6) stands.

This is where the adjudication order raises its most debatable point. The Adjudicating Officer held that a designated existing account does not satisfy the requirement of a 'separate bank account' under Section 42(6). However, as I examine more carefully in Part IX of this article, the bare text of Section 42(6) — as quoted by the ROC itself — does not actually use the word 'open' or 'new.' This interpretational question deserves closer scrutiny, and I would encourage the reader to reserve their final view until Part IX.

Violation 2: Incomplete MGT-14 and Revised Filing After Four Months

The initial MGT-14 filed on 14th February 2025 lacked a complete explanatory statement as required under applicable rules. While the company did file a revised MGT-14, it came on record only on 11th June 2025. This delay is significant.

Violation 3: PAS-4 Circulated Before MGT-14 Filing

The PAS-4 (offer letter) was circulated on 12th February 2025 — the same day as the special resolution — before the MGT-14 was even filed. The proper procedure requires that the offer letter be issued only after compliance with the filing requirements.

Part V: The Company's Defence — And Why It Failed

The company and its directors put up a spirited defence. Let us examine each argument they raised and understand why the Adjudicating Officer rejected them.

Defence 1: "We were misguided by professionals." The company stated that initial professionals told them the resolutions were not as per the Act and that separate bank account meant a new account. They later obtained a PCS opinion saying they were compliant. The ROC did not accept this as a defence — ignorance of law, even if induced by professional advice, does not exempt a company from statutory compliance.

Defence 2: "The designated account effectively served as a separate account." The company argued that since it had designated a specific account (other than its regular cash credit account) and had informed its bank, the spirit of the law was complied with. The ROC disagreed and upheld the violation.

Defence 3: "Minor delay in filing forms due to attachment limitations." The company blamed technical limitations on the MCA portal for delays in filing forms. While this may be a valid operational challenge, it does not constitute a legal defence for non-compliance.

Defence 4: "The e-SCN was generated for Rs. 2 crores, which is higher than the amount raised." This was actually a valid legal point that the company raised and the Adjudicating Officer accepted. The show-cause notice was generated for Rs. 2,00,00,000 (the maximum), but since the amount raised (Rs. 73,44,000) is lower, the penalty was correctly reduced to Rs. 73,44,000 per person. Credit must be given — the company's representative raised this correctly, and the ROC acknowledged it.

Request for minimum penalty: The company and its directors prayed for minimum penalty. The Adjudicating Officer did not grant this either. The penalty imposed equals the full amount raised through the private placement.

Defenses Raised by the Company and Directors (table)

In their reply dated 8th April 2026 and during the e-hearing conducted on 20th April 2026, the company and its directors raised the following defenses:

| S. No. | Defense Argument | Adjudicating Officer's Rejoinder |

|---|---|---|

| 1. | The company was undergoing pre-IPO due diligence. A professional highlighted certain procedural lapses, and the company voluntarily applied for adjudication in good faith. | Voluntary disclosure does not absolve liability. The contravention had already been committed prior to the application. |

| 2. | The company designated one of its existing bank accounts (not the regular CC account) exclusively for this private placement and informed Axis Bank accordingly. | The statutory language employs the word "separate" which, in legal parlance, means a distinct and newly opened account. A repurposed existing account does not satisfy this requirement. |

| 3. | The company was misguided by certain professionals who opined that "separate bank account" does not necessarily mean a "new bank account." | Ignorance of law or reliance on incorrect professional advice is not a valid defense. The directors, as officers in default, bear primary responsibility for ensuring statutory compliance. |

| 4. | Subsequently, a Practicing Company Secretary furnished an opinion confirming compliance with Section 42. | This opinion was obtained after the issuance of the show cause notice. Post-facto compliance certifications do not erase the original violation. |

| 5. | There was no mala fide intention on the part of the company or its directors. | Section 42 creates strict liability. The presence or absence of intention is irrelevant for determining contravention. |

All defenses were rejected by the Adjudicating Officer, and the violation was held to be proved on record.

Part VI: The Penalty — Who Pays, How Much, and When

This is where the severity of the order truly sinks in. The Adjudicating Officer has imposed a penalty of Rs. 73,44,000 (Rs. 73.44 lakhs) each on:

| S.No. | Person | Amount of Penalty |

|---|---|---|

| 1 | Digilogic Systems Limited (Company) | Rs. 73,44,000 |

| 2 | Madhusudhan Varma Jetty (Director) | Rs. 73,44,000 |

| 3 | Radhika Varma Jetty (Director) | Rs. 73,44,000 |

| 4 | Jetty Shashank Varma (Director) | Rs. 73,44,000 |

| 5 | Hitesh Varma Jetty (Director) | Rs. 73,44,000 |

| Total | Rs. 3,67,20,000 |

Key directions in the order:

- The penalty must be paid within 90 days of receipt of the order.

- Payment must be made via the e-Adjudication facility on the MCA portal through respective login IDs.

- The penalty imposed on directors must be paid from their personal sources/income — not from company funds.

- An appeal can be filed before the Regional Director, Hyderabad within 60 days of receipt of the order, in Form ADJ, with a certified copy of the order.

- Non-payment within the prescribed time attracts further consequences under Section 454(8) of the Companies Act, 2013.

Think about this for a moment. The company raised Rs. 73.44 lakhs through private placement. The total penalty imposed across all parties is Rs. 3.67 crores — approximately five times the amount raised. This is the cost of non-compliance.

Part VII: Key Lessons for CS Students and Practitioners

This case offers a goldmine of practical learning. Here are the lessons I would draw as a fellow CS student:

Lesson 1: "Separate Bank Account" — Take It Literally

The most critical takeaway from this case is the interpretation of "separate bank account" under Section 42(6). The company's PCS gave an opinion that a designated account suffices. The ROC disagreed. Until there is a higher judicial clarification to the contrary, the safest advice is: open a new, dedicated bank account specifically for private placement proceeds. Do not use an existing account, however designated it may be. When advising clients, this is the conservative, safe position to take.

Lesson 2: Timing of PAS-4 Is Not Optional

The PAS-4 (Private Placement Offer Letter) must be issued after the filing of Form MGT-14. Circulating the offer letter on the same day as the special resolution, before even filing the MGT-14, is a procedural violation. Maintain the correct sequence: Special Resolution → MGT-14 filing → PAS-4 issuance → Collection of applications (PAS-5) → Allotment → PAS-3 filing.

Lesson 3: IPO Due Diligence Often Reveals Past Non-Compliance

This case is a textbook example of how IPO due diligence digs up skeletons from the past. If you are advising a company eyeing a public issue, conduct thorough secretarial audits of all past private placements — not just the most recent one. Regularise what can be regularised before you file the DRHP. Self-reporting (as this company did through the adjudication application) may show good faith, but it does not guarantee immunity from penalty.

Lesson 4: Self-Adjudication Does Not Guarantee a Lower Penalty

The company proactively filed an adjudication application (dated 30th December 2025, submitted to ROC on 6th January 2026) under Section 454. This is commendable — it shows corporate responsibility. However, as this order shows, self-reporting does not automatically translate to a lower penalty. The ROC imposed the full amount without any reduction for good faith reporting.

Lesson 5: Directors Pay From Their Own Pockets

The order explicitly states that the penalty on officers in default shall be paid from their personal sources/income. This is not a company expense. Four individual directors will each have to pay Rs. 73.44 lakhs from their personal funds. This should serve as a powerful reminder to every director who signs board resolutions without applying their mind to compliance.

Lesson 6: Understand the Penalty Structure of Section 42(10)

The penalty under Section 42(10) is the lower of (a) the amount raised through private placement, or (b) Rs. 2 crores. This company raised only Rs. 73.44 lakhs, so the penalty is Rs. 73.44 lakhs per person. Had the company raised Rs. 3 crores, the penalty would have been capped at Rs. 2 crores per person. Know this structure cold — it appears in exams and in practice.

Lesson 7: Get Your Explanatory Statement Right the First Time

The incomplete MGT-14 — and the four-month delay before a corrected version was accepted — contributed to the overall picture of non-compliance. The explanatory statement under Rule 13 of the Companies (Share Capital and Debentures) Rules, 2014 must contain prescribed information. Do not file a deficient form and expect to fix it later without consequences.

Part VIII: A Note on the Procedural Aspects of Adjudication

From a procedural standpoint, this order is instructive about how adjudication works:

-

Adjudication Application: The company voluntarily filed an adjudication application, acknowledging violations and seeking to regularise them.

-

e-SCN: The ROC issued an electronic Show Cause Notice (e-SCN) dated 27th March 2026 to the company and its officers in default.

-

Reply: The company submitted a reply dated 8th April 2026.

-

e-Hearing: An electronic hearing was conducted on 20th April 2026, at which Madhusudhan Varma Jetty represented the company and other officers.

-

Post-Hearing Submission: Even after the e-hearing, the company submitted a letter dated 20th April 2026 pointing out that the penalty should be capped at Rs. 73,44,000, not Rs. 2 crores. This was accepted.

-

Order: The final adjudication order was issued on 22nd April 2026.

The entire process from adjudication application (06.01.2026) to final order (22.04.2026) took approximately three and a half months. This is relatively swift, and credit goes to the e-adjudication infrastructure of MCA.

Part IX: A Critical Reading — Does Section 42(6) Actually Require Opening a New Bank Account?

As a CS Executive student studying this order, one observation stood out to me that I believe deserves serious attention — and I raise it purely from an academic and analytical standpoint, not as a professional opinion.

The Adjudicating Officer held that the company violated Section 42(6) because it did not open a new separate bank account for receiving private placement proceeds. The company instead designated an existing non-operational account, backed by a board resolution dated 14th September 2024 and written intimation to Axis Bank.

Now here is what struck me.

The ROC itself quoted Section 42(6) verbatim in the order. And that quoted text reads:

"monies received on application under this section shall be kept in a separate bank account in a scheduled bank and shall not be utilised for any purpose other than — (a) for adjustment against allotment of securities; or (b) for the repayment of monies where the company is unable to allot securities."

Reading this carefully — as a student learning statutory interpretation — I notice that the provision uses the words "kept in." It does not say "open a new," "create a fresh," or "establish a dedicated" bank account. The word "open" simply does not appear in Section 42(6).

This raises a genuine question of statutory interpretation:

Does "separate bank account" mean a newly opened account — or does it mean an account that is functionally separate from regular operations?

I am not in a position to answer this definitively as a student. But I would humbly submit the following observations for academic consideration:

1. Plain meaning of "separate" The word "separate" in ordinary English means distinct from or not mixed with something else. It does not inherently mean newly created. A bank account that is not the company's regular operational account, designated exclusively for a specific purpose, is — on a plain reading — "separate."

2. The purpose of the provision The obvious legislative intent behind Section 42(6) is to ringfence investor money — ensuring that application money is not mixed with operational funds and is not misused before allotment. The company in this case:

- Used a non-operational account exclusively

- Did not utilise the money for any other purpose before allotment

- Had a board resolution designating the account in advance

- Had informed Axis Bank of the designation

If the purpose of the provision is investor protection through ringfencing — and that purpose was demonstrably achieved — it is an interesting question whether the technical form (new vs. designated account) should override substantive compliance.

3. The absence of any rule specifying "new account" Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014 — which governs private placement in detail — does not, to my reading as a student, specify that the separate bank account must be a newly opened one. When neither the parent Act nor the subordinate rules make this explicit, it raises the question of whether the Adjudicating Officer has read an obligation into the statute that the legislature did not expressly impose.

4. Strict construction of penal provisions It is a well-settled principle that penal provisions must be strictly construed — meaning that if there is ambiguity, it must be resolved in favour of the person being penalised. I humbly submit that there is at least arguable ambiguity here about what "separate bank account" means, and that principle of strict construction would suggest that ambiguity should favour the company.

I want to be clear — I raise these points as a student engaging in academic analysis of a publicly available government order, not as a legal or professional opinion. I may be wrong. There may be judicial precedents or MCA circulars that settle this question in favour of the ROC's interpretation that I am not yet aware of.

But I believe that asking these questions — going back to the bare text, examining what the law actually says versus what an authority assumes it says — is precisely the kind of critical thinking that the CS profession needs more of.

If any senior professional, PCS, or advocate reading this has a view on this interpretational question, I would genuinely welcome their perspective in the comments.

Conclusion: Compliance Is Cheaper Than Penalties

The Digilogic Systems case is ultimately a cautionary tale about the cost of cutting corners in private placement compliance. A company preparing for an IPO — a milestone that involves enormous aspirations and years of work — found itself paying over Rs. 3.67 crores in total penalties for procedural lapses in a transaction worth Rs. 73.44 lakhs.

The irony is not lost: the company raised Rs. 73.44 lakhs and ended up paying a collective penalty of nearly five times that amount. The cost of opening a separate bank account, filing a complete MGT-14 on time, and following the correct sequence for PAS-4 issuance would have been negligible. The cost of not doing so has been enormous.

As future Company Secretaries, we are the last line of defence against such outcomes. Our role is not merely to file forms — it is to build compliance cultures within organisations, to ask the difficult questions, and to ensure that no transaction is completed without ticking every statutory box. The law in this area is exacting and the penalties are severe.

Study this order. Save it. And the next time someone tells you that a designated account is "essentially the same" as a separate bank account — remember Digilogic Systems Limited.

Conclusion for Examination Purpose

For my CS Executive and Professional exams, I will remember this case as the "Separate Bank Account Case."

The one-line takeaway:

If you use an old bank account for private placement, even with good intention, you violate Section 42(6), and penalty under Section 42(10) will be levied on the company and every director to the extent of the amount raised (or ₹2 crore, whichever is lower).

Penalty formula to memorize:

*Penalty = Lower of (Amount Raised OR ₹2 Crore) × (Company + Number of Directors/Promoters in default)*

In this case: ₹73,44,000 × 6 persons = ₹3,67,20,000

This article is written from an academic and educational perspective by a Company Secretary student, for the purpose of understanding adjudication orders under the Companies Act, 2013. All facts are sourced from the adjudication order issued by ROC Hyderabad bearing Order ID PO/ADJ/04-2026/HD/02037 dated 22nd April 2026.