What is Section 112 of the Income Tax Act?

Section 112 provides for tax on Long-Term Capital Assets. It applies to all taxpayers such as individuals, HUFs, partnership firms, companies, residents, non-residents, foreign companies, etc. This section covers capital gains arising from the sale of all long-term capital assets. Long Term Capital Asset covers the following assets:

1. Securities (other than units) listed on a recognized stock exchange in India

2.Unit of the unit trust of India

3.Zero-coupon bond

4.Securities not listed on a recognized stock exchange in India

5.Immovable property being land, building, or both

6.Any other capital asset.

Computation of tax on LTCG on transfer of land or building or both on or after 23.7.2024 [Section 112]

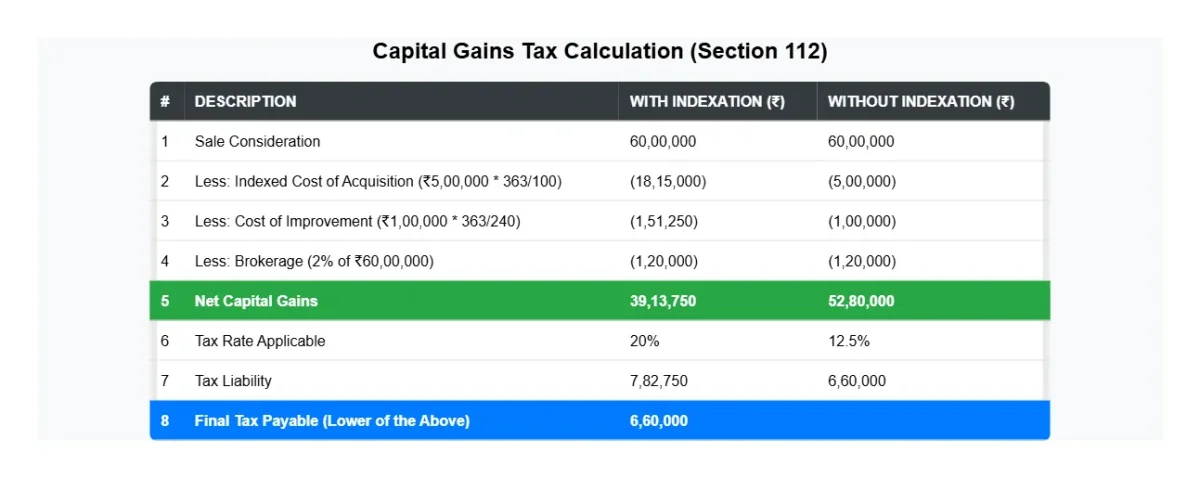

A resident individual or HUF, while computing tax on LTCG on transfer of land or building or both, has the option to take the benefit of indexation under section 112 in respect of long-term capital gains arising on transfer of land or building or both which is acquired before 23.7.2024 and transferred on or after 23.7.2024. Accordingly, LTCG on transfer of such land or building or both are subject to lower of tax @12.5% (on LTCG computed without indexation benefit) or @20% (on LTCG computed with indexation benefit).

(Note:- Indexation benefits are allowed only on land and building acquired before 23/07/2024 and Holding pered more than 24 months not on other long-term assets.)

It may be noted that this benefit to a resident individual or HUF is to be given only while computing tax on LTCG under section 112 on transfer of land or building or both and not while computing Income under the head “Capital Gains” which would form part of gross total income/total income. Thus, for computing income under the head “Capital Gains” to be included in gross total income, indexation benefit is not to be giveneven in case of resident individual/HUF transferring land or building or both on or after 23.7.2024 which was acquired after 23.7.2024. (See the Question 2 with Working Note)

Value of consideration (Section 50C)

Where the consideration received or accruing as a result of the transfer by an assessee of a capital asset, being land or building or both, is less than the value adopted or assessed or assessable by any authority of a State Government (hereafter in this section referred to as the “stamp valuation authority”) for the purpose of payment of stamp duty in respect of such transfer, the value so adopted or assessed or assessable shall, for the purposes of section 48, be deemed to be the full value of the consideration received or accruing as a result of such transfer :

(In simple terms:- If the selling price of land or building is less than the stamp duty value set by the government, then the stamp duty value will be considered as the selling price for calculating capital gains tax under Section 48.)

Provided that where the date of the agreement fixing the amount of consideration and the date of registration for the transfer of the capital asset are not the same, the value adopted or assessed or assessable by the stamp valuation authority on the date of agreement may be taken for the purposes of computing full value of

(In Simple terms :- If the sale agreement date and registration date are different, the stamp duty value on the agreement date can be used to calculate the full value of consideration, instead of the value on the registration date.)

consideration for such transfer: Provided further that the first proviso shall apply only in a case where the amount of consideration, or a part thereof, has been received by way of an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account or through such other electronic mode as may be prescribed, on or before the date of the agreement for transfer:

(In Simple terms :-The stamp duty value on the agreement date can be used only if the buyer has paid full or partial consideration through account payee cheque, bank draft, electronic transfer, or other prescribed modes on or before the agreement date (if Buyer pay the Consideration after date of agreement Can not Consider)

Example:

Before the Agreement Date (Eligible for Agreement Date Stamp Duty Value)

Suppose Mr. A agrees to sell his land to Mr. B for ₹50 lakh on 1st June 2024, and the stamp duty value on this date is ₹55 lakh. Mr. B makes an advance payment of ₹10 lakh via an account payee cheque on 31st May 2024. The final sale deed is registered on 1st August 2024, when the stamp duty value has increased to ₹60 lakh. Since part of the payment was made before the agreement date through a valid banking mode, Mr. A can use the stamp duty value of ₹55 lakh (as on the agreement date) for calculating capital gains instead of ₹60 lakh.

After the Agreement Date (Cannot Use Agreement Date Stamp Duty Value)

Now, suppose Mr. A and Mr. B signed the same agreement on 1st June 2024, but Mr. B paid the ₹10 lakh advance only on 5th June 2024 (after the agreement date). In this case, Mr. A cannot use the stamp duty value of ₹55 lakh from the agreement date. Instead, he must use the ₹60 lakh stamp duty value from the registration date for capital gains calculation.

Provided also that where the value adopted or assessed or assessable by the stamp valuation authority does not exceed one hundred and ten per cent of the consideration received or accruing as a result of the transfer, the consideration so received or accruing as a result of the transfer shall, for the purposes of section 48, be deemed to be the full value of the consideration

(In Simple terms:-If the stamp duty value is not more than 110% of the actual selling price, then the actual selling price will be used for capital gains calculation instead of the stamp duty value.)

Example:

- Case 1 (Stamp Duty Value Within 110%) – No Adjustment Needed

Mr. A sells his land for ₹50 lakh, and the stamp duty value is ₹54 lakh. Since ₹54 lakh is within 110% of ₹50 lakh (i.e., ₹55 lakh), the actual selling price of ₹50 lakh will be used for capital gains calculation. - Case 2 (Stamp Duty Value Exceeds 110%) – Adjustment Required

Mr. A sells his land for ₹50 lakh, but the stamp duty value is ₹58 lakh. Since ₹58 lakh exceeds 110% of ₹50 lakh (i.e., ₹55 lakh), the higher stamp duty value of ₹58 lakh will be used for capital gains calculation instead of ₹50 lakh.

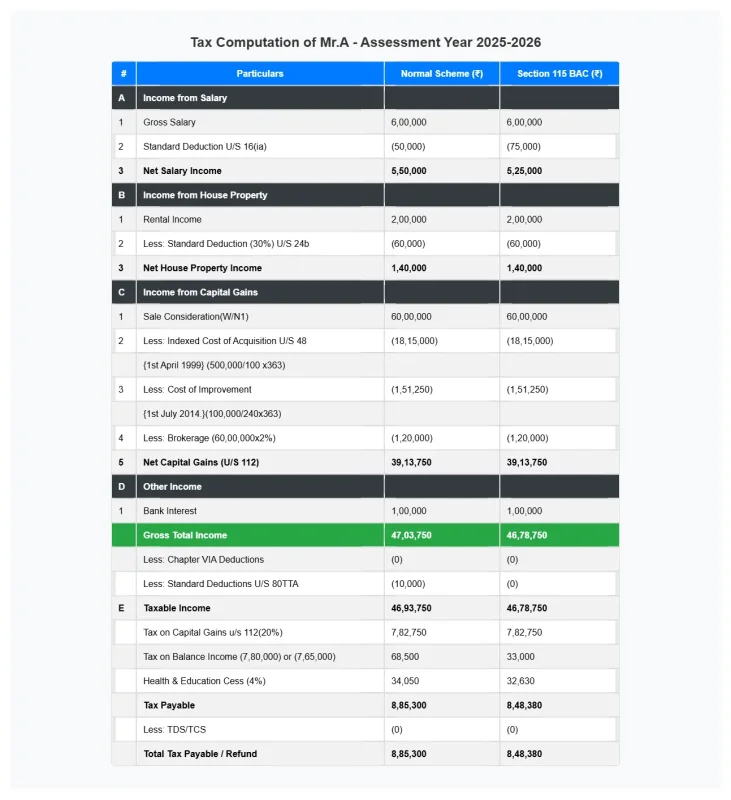

Question: 1

Mr. A, a resident of India, acquired a property on 1st April 1999 for ₹5,00,000. He incurred an improvement expense of ₹1,00,000 on 1st July 2014. He sold the property on 25th June 2024 for ₹60,00,000, and paid brokerage @2% of the sale value. The stamp duty value on the sale date was ₹65,00,000.

In addition to this, Mr. A has the following other income:

- Salary Income: ₹6,00,000

- House Property Income: ₹2,00,000

- Bank Interest: ₹1,00,000

Compute the total taxable income and tax liability (Default Tax Regime and Regular Tax Regime) of Mr. A for Assessment Year 2025-26, considering that the sale was made before 23rd July 2024.

Working Note 1: Section 50C – Consideration for Capital Gains Calculation

As per Section 50C of the Income Tax Act, if the stamp duty value (SDV) is not more than 110% of the actual sale consideration, the actual sale price will be considered for capital gains computation.

Given Data:

- Sale Consideration (Actual Selling Price) = ₹60,00,000

- Stamp Duty Value (SDV) = ₹65,00,000

- 110% of Sale Consideration = ₹60,00,000 × 110% = ₹66,00,000

Applicability of Section 50C:

Since the SDV (₹65,00,000) is less than ₹66,00,000, the actual sale price of ₹60,00,000 will be considered for capital gains calculation.

Final Consideration for Capital Gains Calculation:

✅ Sale Consideration (as per law) = ₹60,00,000

This means the stamp duty value will not be considered, and capital gains will be computed based on ₹60,00,000.

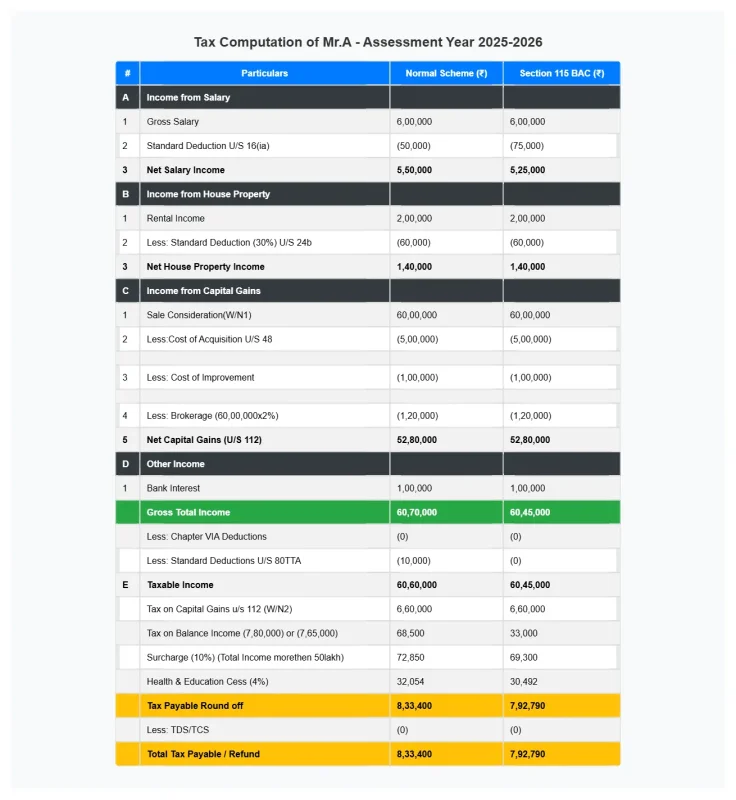

Question: 2

Mr. A, a resident of India, acquired a property on 1st April 1999 for ₹5,00,000. He incurred an improvement expense of ₹1,00,000 on 1st July 2014. He sold the property on 25th September 2024 for ₹60,00,000, and paid brokerage @2% of the sale value. The stamp duty value on the sale date was ₹65,00,000.

In addition to this, Mr. A has the following other income:

- Salary Income: ₹6,00,000

- House Property Income: ₹2,00,000

- Bank Interest: ₹1,00,000

Compute the total taxable income and tax liability (Default Tax Regime and Regular Tax Regime) of Mr. A for Assessment Year 2025-26, considering that the sale was made After 23rd July 2024.

Working Note 1: Section 50C – Consideration for Capital Gains Calculation

As per Section 50C of the Income Tax Act, if the stamp duty value (SDV) is not more than 110% of the actual sale consideration, the actual sale price will be considered for capital gains computation.

Given Data:

- Sale Consideration (Actual Selling Price) = ₹60,00,000

- Stamp Duty Value (SDV) = ₹65,00,000

- 110% of Sale Consideration = ₹60,00,000 × 110% = ₹66,00,000

Applicability of Section 50C:

Since the SDV (₹65,00,000) is less than ₹66,00,000, the actual sale price of ₹60,00,000 will be considered for capital gains calculation.

Final Consideration for Capital Gains Calculation:

✅ Sale Consideration (as per law) = ₹60,00,000

This means the stamp duty value will not be considered, and capital gains will be computed based on ₹60,00,000.